Success strategies for efficient spare parts logistics

Optimize your spare parts logistics with digital strategies, efficient distribution networks and modern warehouse management…

blog

The US industry is changing: growth regions are emerging, traditional centers are transforming. Take advantage of these opportunities as an industrial company! We show you the most attractive locations, plan investments based on data and ensure your long-term success – whether in mechanical engineering, automotive, chemicals, high-tech or food production.

The USA is a key market for industrial companies from the DACH region. In view of global trade changes, many companies are increasingly focusing on a “local for local” strategy – production in the USA for the US market. Choosing the right

The real gross value added of the US manufacturing industry grew from USD 2.3 trillion in 2019 to USD 2.9 trillion in 2024. USD to 2.9 trillion. USD – an annual growth rate of around 4.3 % (U.S. Bureau of Economic Analysis). This sector includes mechanical engineering, the automotive industry, chemicals and electronics – precisely the industries in which companies from the DACH region are traditionally strong.

In this article, we show which US regions are particularly attractive, which location conditions are decisive and how companies can identify dynamic opportunities for investment and growth.

Choosing the right location raises key questions:

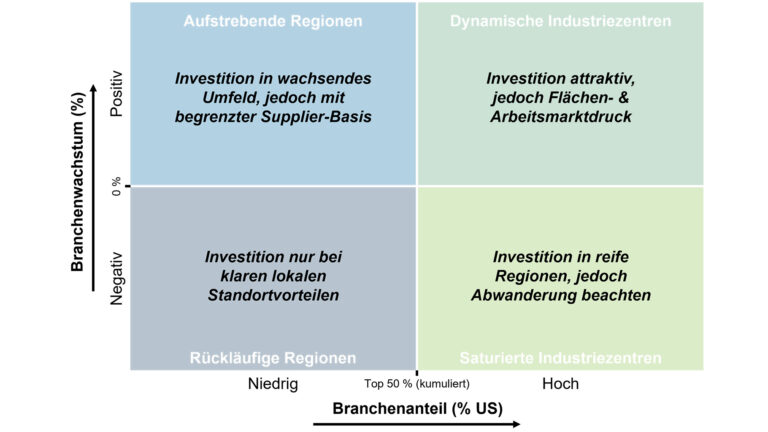

Our framework for evaluating US regions shows industry growth on the vertical axis and the industry share on the horizontal axis.

Industry growth (Y-axis) is the dynamic component of our analysis. It shows the extent to which a US state has experienced positive or negative growth in a specific industry, such as the chemical industry, over the past five years. For the calculation, we used data from the U.S. Census Bureau and looked at the total number of employees in an industry between 2019 and 2023. The absolute change in the number of employees is a good indicator of industry growth, as productivity improvements over a period of just five years are hardly significant.

The industry share (x-axis) represents the static component. It shows the absolute size of an industry in a federal state based on the number of employees. For a better overview, we focus on the states that together account for 80 % of the number of employees in an industry. To the right of the axis label “50 % US share” (see Figure 1) are the states that together cover a maximum of 50 % of employees; to the left are the remaining 50 % to 80 %. The number of states shown varies depending on the industry. For example, the automotive industry only covers nine states, as this industry is heavily concentrated in the Great Lakes region (Michigan, Indiana, Ohio alone account for 40%).

The combination of the two dimensions results in four quadrants with corresponding recommendations.

Dynamic industrial centers: States in this quadrant are characterized by considerable industry strength and dynamic economic growth. Risk-averse companies in particular can invest here, as they can expect a good infrastructure, a stable supply network, a well-trained workforce and a high quality of life. At the same time, it should be noted that these industrial centers may reach their capacity limits in the long term, leading to growing competition for space and workers. The low risk is therefore accompanied by a higher cost structure for investing companies.

Declining regions: States in this quadrant have only a small industry base and are in economic stagnation. Investments should only be made here if there are clear local locational advantages, such as subsidies, proximity to suppliers, existing buildings that can be taken over or proximity to the market (e.g. in the food industry). Otherwise, the risks outweigh the benefits, as the region’s dynamism is limited and the chances of growth are low.

Emerging regions: States in this quadrant are experiencing strong economic growth with a moderate industrial density to date. They are particularly interesting for companies that want to benefit from the regional upturn at an early stage. These developments often go hand in hand with growth-friendly framework conditions such as local subsidies, population growth and moderate location costs – although these may rise in the medium term. For risk-tolerant companies that are not heavily dependent on individual customers and can flexibly establish new supply chains, long-term development opportunities and an attractive environment for employees are offered here.

Saturated industrial centers: States in this quadrant have a high proportion of industry, but are experiencing a decline in industrial activity, often accompanied by population decline (such as in the Rust Belt, particularly in automotive and heavy industry) and at the same time continuing high wage levels. Investment in these mature regions is possible, but should take into account the migration of companies and skilled workers. For companies that are heavily dependent on individual customers or a well-developed supplier network, the location can still be interesting, as existing structures and supply chains provide a solid basis for operational activities.

In the following, we focus on the individual sectors and their most important regions.

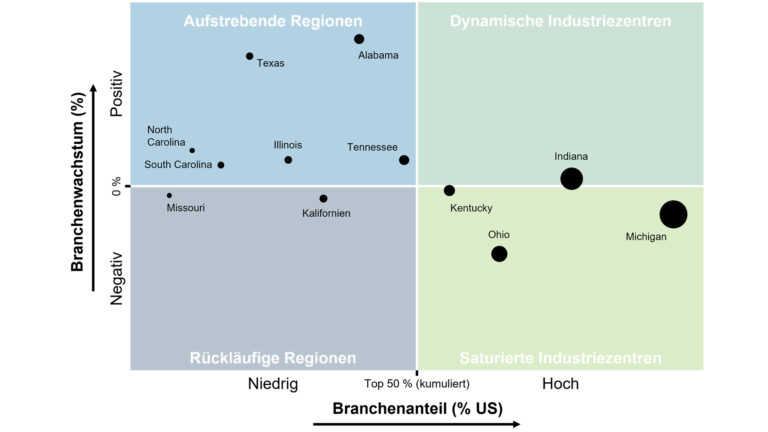

The automotive sector is characterized by high capital intensity, a large number of variants and the use of state-of-the-art manufacturing technologies. Historically, strong automotive clusters have developed in the USA in the so-called “Rust Belt” (Detroit and southern Midwest), in which OEMs and suppliers have been able to realize efficient just-in-time/just-in-sequence supply chains in a comprehensive ecosystem. The American automotive industry employs over 800,000 people. Tesla operates the largest factories: around 20,000 employees work in Fremont (CA) and Austin (TX). Other major production sites include BMW in Spartanburg (SC) with 11,000 employees as well as Ford (Claycomo, MO and Louisville, KY), Toyota (Georgetown, KY and Princeton, IN) and Nissan (Smyrna, TN) plants, which each employ more than 7,000 people.

As Figure 2 shows, the Great Lakes states remain very important in the automotive industry. The three states of Michigan, Indiana and Ohio alone account for around 40 % of jobs in the automotive industry, including at global OEMs such as Honda, Ford, Stellantis, Toyota and GM as well as at important suppliers from the DACH region such as Bosch, Continental, ZF and Mahle.

At the same time, however, the matrix also shows the challenges that apply to many Rust Belt states: comparatively high wages, older plants, population decline, structural change and the strong influence of trade unions have led to stagnating growth. This is particularly evident in Michigan (-0.8 % p.a.) and Ohio (-1.9 % p.a.) in recent years.

In contrast, regions in the emerging “Southern Auto Corridor” (Alabama, Tennessee, North and South Carolina, Texas) are recording strong growth. Here, companies are benefiting from lower labor costs, more flexible labor markets and extensive government subsidies.

Alabama in particular has developed into a leading automotive location: The state was the No. 1 auto exporter in the U.S. for the first time in 2023, with exports totaling more than $11 billion, a 45% increase since 2021. The industrial base in Alabama has gained significant momentum in recent years: The plants of Mercedes-Benz in Tuscaloosa (6,100 MA), Hyundai in Montgomery (3,500 MA) and Mazda-Toyota in Huntsville (4,000 MA) have expanded their capacities. At the same time, numerous suppliers such as ZF, Bosch, Brose, Dräxlmaier, MANN+HUMMEL and Continental have settled or expanded in the region. One example of current investments is Toyota: the company launched the production of a new engine at its plant in Huntsville with a USD 280 million project. Hyundai also invested USD 290 million to expand SUV production in Montgomery.

In 2023, Alabama set a milestone and became the largest car exporter in the USA for the first time – a symbol of the dynamism of the Southern Auto Corridor.

Dr. Jens Kaiser, Senior Consultant

In addition, the Southern Auto Corridor has developed into a center of electromobility: Tesla employs around 20,000 employees in its Gigafactory in Austin (TX), while BMW in Spartanburg (11,000 employees) is increasingly producing hybrids (including the X3 and X5 for the global market) and VW in Chattanooga (5,500 employees) is manufacturing electric vehicles (including the ID.4 SUV). These investments have resulted in numerous battery and component plants – such as Toyota’s USD 1.3 billion investment in Kentucky or the new Hyundai battery plant in Georgia. The industrial presence in the South is complemented by VW, which has started construction of the Scout plant in Columbia (SC).

The southern US is thus developing into a new industrial powerhouse, while the Rust Belt, with its strong industrial base, experienced workforce and existing supply networks, continues to play a key role in the transformation process – especially for re-tooling, electrification of existing plants and the integration of supplier networks from Europe.

Mechanical engineering is characterized by a broad product portfolio and numerous customer-specific solutions. This requires high levels of investment in machinery, tools and production infrastructure. Due to the high proportion of personnel and material costs, many companies prefer locations with competitive wage structures and a strong supplier base. Manufacturers often work closely with their suppliers on product design and engineering. In order to meet the diverse customer requirements, production is often strongly engineering and project-oriented. Access to technical expertise – whether through technology clusters or well-trained specialists – is essential for the industry.

The American mechanical engineering sector employs around 1.1 million people and generates sales of around USD 450 billion. The segments with the highest turnover include heating, ventilation and air conditioning technology (USD 65 billion), followed by construction machinery, conveyor technology and engines and power units (approx. USD 50 billion each).

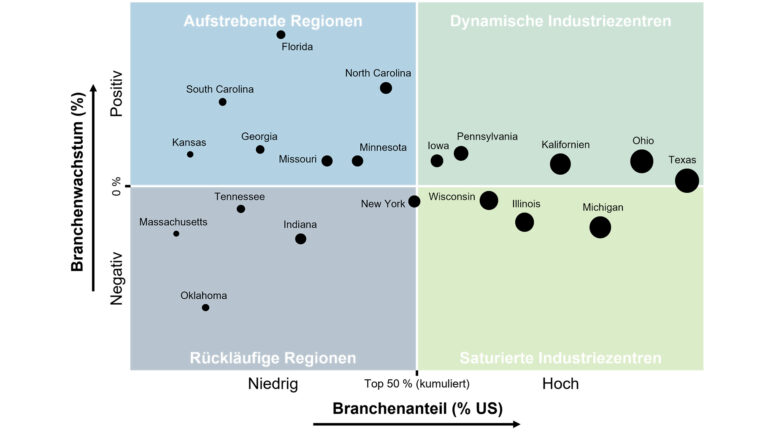

As our analysis shows (see Figure 3), unlike the automotive industry, no clearly definable regional clusters have formed in the mechanical engineering sector. The industry is comparatively evenly distributed across the entire USA. Overall, the sector is growing rather slowly – in fact, it is the slowest growing of the five industries analyzed. However, after a slight decline in 2023 and 2024, experts expect moderate growth in the coming years.

The largest production centers are located in Texas (including Caterpillar), California (including Haas Automation) and the Great Lakes states (including GE Aerospace, John Deere, Caterpillar). These established industrial centers are moving within a moderate growth range of -1 % to +0.7 % p.a.

Florida and the Carolinas are showing strong production growth. In Florida, power generation (Siemens Energy, Siemens Gamesa, Mitsubishi Power, GE Vernova) and aviation technology (GE Aerospace, Pratt & Whitney) are the main drivers of mechanical engineering. In the Carolinas, investments such as the expansion of the factory of Crailsheim-based filling machine manufacturer Groninger (+60 employees) and the opening of a new production facility by Canadian packaging specialist AVL Manufacturing (+325 employees) confirm the trend. DEHN, a German manufacturer of lightning and surge protection systems, is also planning an investment of around USD 40 million in Mooresville (NC) and will create around 200 new jobs there by 2029. The region around Charlotte chosen by the aforementioned companies scores points with its excellent infrastructure, connections to Charlotte International Airport and the Port of Charleston.

Oklahoma, on the other hand, loses around 3% of mechanical engineering jobs each year (approx. 750 jobs) due to its high dependence on the oil and gas industry. One example: the closure of the Halliburton site in El Reno in 2019 cost around 800 jobs in the production of fracturing equipment.

As DEHN and Groninger show, the Carolina states offer medium-sized mechanical engineering companies ideal opportunities to establish new production sites and create jobs.

Dr.-Ing. Kai Philipp Bauer, Senior Manager

The chemical industry mainly comprises standardized products as well as some specialty products. In addition to good access to raw materials, low energy costs, a skilled workforce and proximity to universities and research clusters are key factors in the choice of location. Tax incentives and less stringent environmental regulations also play an important role.

After China, the US chemical industry is the second largest in the world with a turnover of around USD 900 billion (2022). With a share of over 25 % of national GDP, it has significant economic relevance. The industry is heavily export-oriented: Around half of production is exported; for the manufacturing sector as a whole, the US figure is just 29%. Employment growth of over 2% per year shows that the chemical industry is one of the most dynamic sectors of the US economy.

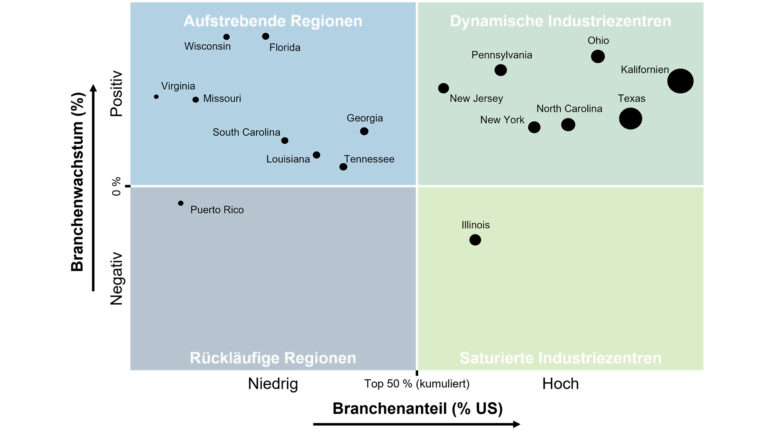

The American chemical industry has been experiencing strong growth for years, with Florida and Wisconsin standing out in particular.

Dr.-Ing. Kai Philipp Bauer, Senior Manager

As Figure 4 shows, the established industrial centers are located in California, Texas, Ohio and along the East Coast (New Jersey, New York, Pennsylvania, North Carolina). These states combine historic industrial clusters, a well-trained workforce and specialized suppliers. Texas benefits from oil and gas deposits for petrochemicals (including BASF, Evonik, Henkel, Lanxess), Ohio and Pennsylvania have a strong basic chemicals tradition (including Bayer, Evonik), while California, North Carolina, New Jersey and New York focus on specialty chemicals, pharmaceuticals and life sciences. Universities and research centers provide innovation, well-developed ports and transportation routes enable efficient logistics, and political incentives encourage investment.

Among the up-and-coming regions, Wisconsin (+3.3% p.a.) and Florida (+3.4% p.a.) stand out. Florida is recording strong industrial growth overall, particularly in the petrochemical sector (including FAR Chemical). Wisconsin has developed into an important location for the chemical and pharmaceutical industry thanks to targeted investments, government support and a strong research landscape. In December 2024, Eli Lilly announced a USD 3 billion expansion of its plant in Kenosha County to produce diabetes and obesity medications and create around 750 new jobs by the end of 2025.

Illinois is the only federal state with a downward trend: The number of employees in the chemical industry here fell by 1.6% annually (approx. 700 employees p.a.). Mass layoffs of over 14,000 people in 2024, including jobs in the chemical industry, indicate a challenging investment environment. High property taxes, corporate taxes and a maximum unemployment insurance contribution of 8.65 % increase operating costs and present additional hurdles for companies.

Overall, the US chemical industry is growing strongly, driven by established clusters in California, Texas, Ohio and on the East Coast as well as emerging regions such as Florida and Wisconsin. The industry benefits from a combination of a skilled workforce, research centers, efficient logistics structures and political incentives that encourage investment and promote innovation.

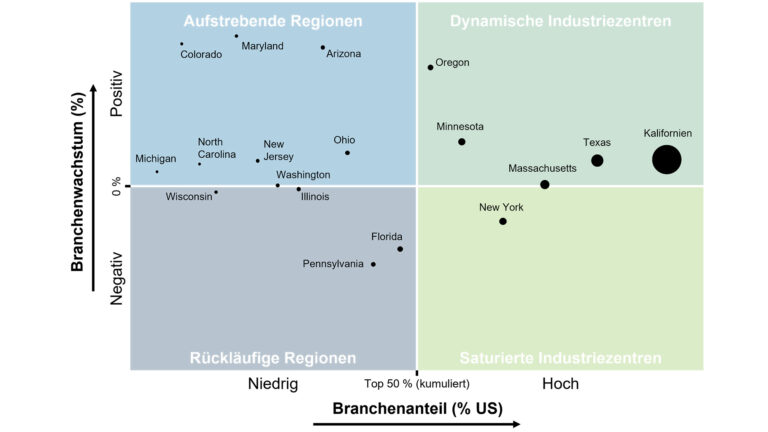

The electronics and high-tech industry is characterized by its innovative strength and precision orientation. For companies looking to invest in this sector, locations that offer access to a good workforce and highly qualified specialists with a short induction period and an innovation-friendly environment are attractive. Ideally, these locations have technology centers such as Silicon Valley (CA) or Austin (TX) as well as renowned universities. In addition, many investors rely on technology promotion programs or other investment initiatives. A high quality of life and a well-developed infrastructure increase the attractiveness for highly qualified employees.

In our analysis, the term “electronics and high-tech” covers companies that manufacture computers, communications equipment, measurement technology and components such as semiconductors and printed circuit boards. More than 800,000 people work in this sector in the USA. As Figure 5 shows, the industry is heavily influenced by California, where a total of around 165,000 people are employed. The most important companies in the state include NVIDIA, Apple, Qualcomm and Advanced Micro Devices (AMD). Together with the next four states – Texas (including Texas Instruments, Dell), Massachusetts (including Mercury Systems), New York (including Universal Instruments Corporation), Minnesota (including IBM, Versa Electronics) and Oregon (including Intel) – a total of 49% of the approximately 800,000 employees nationwide are already employed.

With NVIDIA, Apple and AMD, California is clearly the strongest high-tech location in the USA. But Texas, Minnesota and Oregon are catching up and offer investment opportunities.

Dr. Jens Kaiser, Senior Consultant

Arizona, Maryland and Colorado are among the up-and-coming regions of the US electronics and high-tech industry. In Arizona, billion-dollar investments by companies such as TSMC in Phoenix are driving the expansion of a dynamic semiconductor cluster, supported by targeted funding programs and access to skilled workers. Maryland benefits from its proximity to universities, research institutes and federal authorities and is strengthening small and medium-sized technology companies in particular with smart manufacturing initiatives. In Colorado Springs (CO), investments in semiconductor manufacturing by Microchip Technology (+400 MA) and Entegris (+600 MA) as well as a strong research landscape are fostering the expansion of an innovation-driven high-tech ecosystem. Together, these states stand for new industrial growth beyond the traditional technology regions.

In the electronics and high-tech sector, New York (-1.5 % p.a.), Florida (-2.8 % p.a.) and Pennsylvania (-3.6 % p.a.) are currently showing a downward trend. Although New York is seeing major investment projects such as the Micron Megafab in Clay (construction to start in 2025), high costs and lengthy approval procedures are slowing broader growth. Florida is at odds with its otherwise fast-growing industries such as chemicals and mechanical engineering: while petrochemicals, logistics and construction are expanding strongly, electronics manufacturing remains comparatively weak, even though electronics and PCB manufacturers are growing locally. Pennsylvania has a broad industrial base, but is struggling with ageing infrastructure, a shortage of skilled workers and limited investment incentives, although selective modernization programmes have only partially counteracted this.

Compared to the sectors presented above, the food industry has a significantly lower investment requirement and degree of innovation. In addition to the high proportion of raw material costs, comparatively high transportation costs play a decisive role in overall costs, meaning that companies pay particular attention to proximity to large sales markets and fast, reliable and cost-effective distribution when making investment decisions. At the same time, MAs with good process and supply chain expertise are particularly in demand.

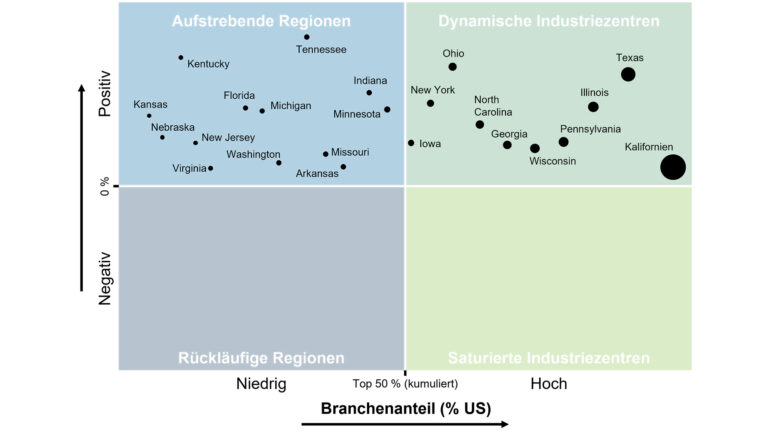

Due to the steady increase in food consumption in the US, the industry is on a continuous growth trajectory. With an annual increase in employees of 1.6% in the years 2019 to 2023, it ranks second behind the chemical industry among the sectors we analyzed. This does not yet take into account the rationalization potential realized through automation, for which Germany is the largest supplier country with a turnover of USD 1.3 billion. Overall, the food industry in the USA generates sales of just under USD 2 trillion. USD.

The American food industry is growing steadily, with populous states such as California, Texas, Illinois and Pennsylvania offering attractive opportunities for sustainable investments.

Dr.-Ing. Kai Philipp Bauer, Senior Manager

Figure 6 clearly shows the industry’s strong growth trajectory. None of the 23 states, which employ 80% of the US workforce in this sector, has recorded a decline over the last five years. The major industry centers are located in states with large populations such as California, Texas, New York, Illinois and Pennsylvania, which together have over 80 million inhabitants. They are also located in logistically favorable locations such as Georgia, North Carolina and Iowa.

Many other states are considered up-and-coming regions. Kentucky and Tennessee stand out in particular, with the highest annual growth rates of 3.2% and 3.7% respectively, creating around 1,200 and 1,600 new jobs per year. Tennessee has implemented around 50 projects in the food and agriculture industry since 2018, creating more than 5,800 new jobs and over USD 2 billion in investment. Companies such as ingredients and systems manufacturer Newly Weds Foods have expanded their production capacities (+50 MA), supported by state funding programs that strengthen the industry’s competitiveness and innovative strength. Kentucky benefits from a strong agricultural base, particularly in meat production, and its central location, which offers logistical advantages. Since 2017, over 300 projects in the food and beverage industry have been announced here, with more than USD 9.4 billion in investment and over 10,200 new jobs. Companies such as meat processor Tyson Foods and the American subsidiary of Japanese ingredients manufacturer Mizkan have expanded their capacities to meet the growing demand.

Senior Manager

With many years of experience in global production strategy and location evaluation, Rothbaum supports you in making data-based, risk-aware and strategically sound investment decisions – for the location that best suits your company size, industry and growth ambitions. We look forward to hearing from you.

Our analysis shows: The location dynamics in the USA vary greatly between established industrial centers, high-growth regions and mature markets undergoing structural change. Large corporations benefit above all from dynamic and emerging regions with access to skilled labor, global supply chains and attractive production conditions – even if this goes hand in hand with higher costs and long-term location commitment. Medium-sized companies, on the other hand, are more risk-conscious and prefer stable networks, predictable framework conditions and familiar industrial ecosystems, for example in established clusters or industrial parks.

We support you in your location decisions with analyses, market knowledge and our local network. We identify potential and risks in the mechanical engineering, toolmaking, automotive, chemical and food industries – and implement the results together with you. In doing so, we rely on our strong local network – from real estate development and the targeted use of subsidies to implementation.

Senior Consultant, Munich

Jens Kaiser studied industrial engineering in Aachen and Beijing and completed his doctorate on the topic of strategic roles of production sites at the University of St. Gallen. He has been working as a consultant for over 5 years, focusing on production networks, production strategy, productivity improvement and supply chain management.

Senior Manager, Hamburg

Kai Philipp Bauer studied mechanical engineering with a focus on production technology and has been working in consulting for over 15 years. He advises his clients in particular on issues relating to strategy development, operations management and digital transformation.

Optimize your spare parts logistics with digital strategies, efficient distribution networks and modern warehouse management…

An automated small parts warehouse (AKL) with shuttle technology offers maximum efficiency, flexibility and storage…

How attractive is Eastern Europe as a production location in 2025? Find out everything you…

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Facebook. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Instagram. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information