The best production locations in the USA at a glance

We show you the best US production locations for mechanical engineering, chemicals, automotive & high-tech.…

BLOG

The USA has voted: Donald Trump will lead the world’s largest economy as the 47th US president until 2028 and his decisions will have a lasting impact on US domestic and foreign policy for years to come. What will the consequences be for European industry? We shed light on how companies can adapt their supply chain strategy to be prepared for potential impacts and risks.

Since November 5, 2024, Donald Trump has been confirmed as President-elect of the USA, making him the second US President to serve a second, non-consecutive term in office. His “America First” strategy is based on protectionist trade policies, particularly towards China and Europe. This US economic policy harbors considerable risks for European industry and could fundamentally change trade relations. Experts such as the IFW Kiel and the BDI speak of an “economically difficult moment” and an “epochal change”.

During his first term in office, Trump drove the growth of the US economy through tax reforms, labor market adjustments and deregulation of the energy, agriculture and financial sectors. Together with Biden’s Inflation Reduction Act, he laid the foundations for continued market growth and the renewed attractiveness of the US for foreign investment.

For his second term in office, Trump has announced that he will increase import tariffs on numerous industrial and consumer goods, further reduce corporate taxes and cut energy costs by increasing subsidies for fossil fuels. “America First” will noticeably change access to the US market. At the same time, manufacturing companies worldwide must be prepared for further effects and adjustments.

Trump’s second term will be a challenge for European industry. Companies will have to adapt their supply chain strategy with foresight. However, it also offers the opportunity to benefit from US market growth.

Dr.-Ing. Kai Philipp Bauer, Senior Manager

Some risks and potentially negative consequences for European industry can be derived from Trump’s first-term policies, his current announcements and his political rhetoric:

Trump has announced that he will impose 10% import tariffs on EU goods, although individual sectors could be affected by even higher tariffs. This would hit the export-oriented German economy in particular and reduce sales on the US market by around 15% according to estimates. However, the extent to which these import duties will affect the prices of foreign products on the US market depends on the development of the EUR/USD exchange rate, among other things. An appreciation of the US dollar could reduce the impact of import duties if companies conclude their sales contracts in US dollars.

There is also the threat of an economic slowdown in China, as Trump could consider tariffs of up to 60% on Chinese imports, which could also further weaken sales of European industrial goods in China.

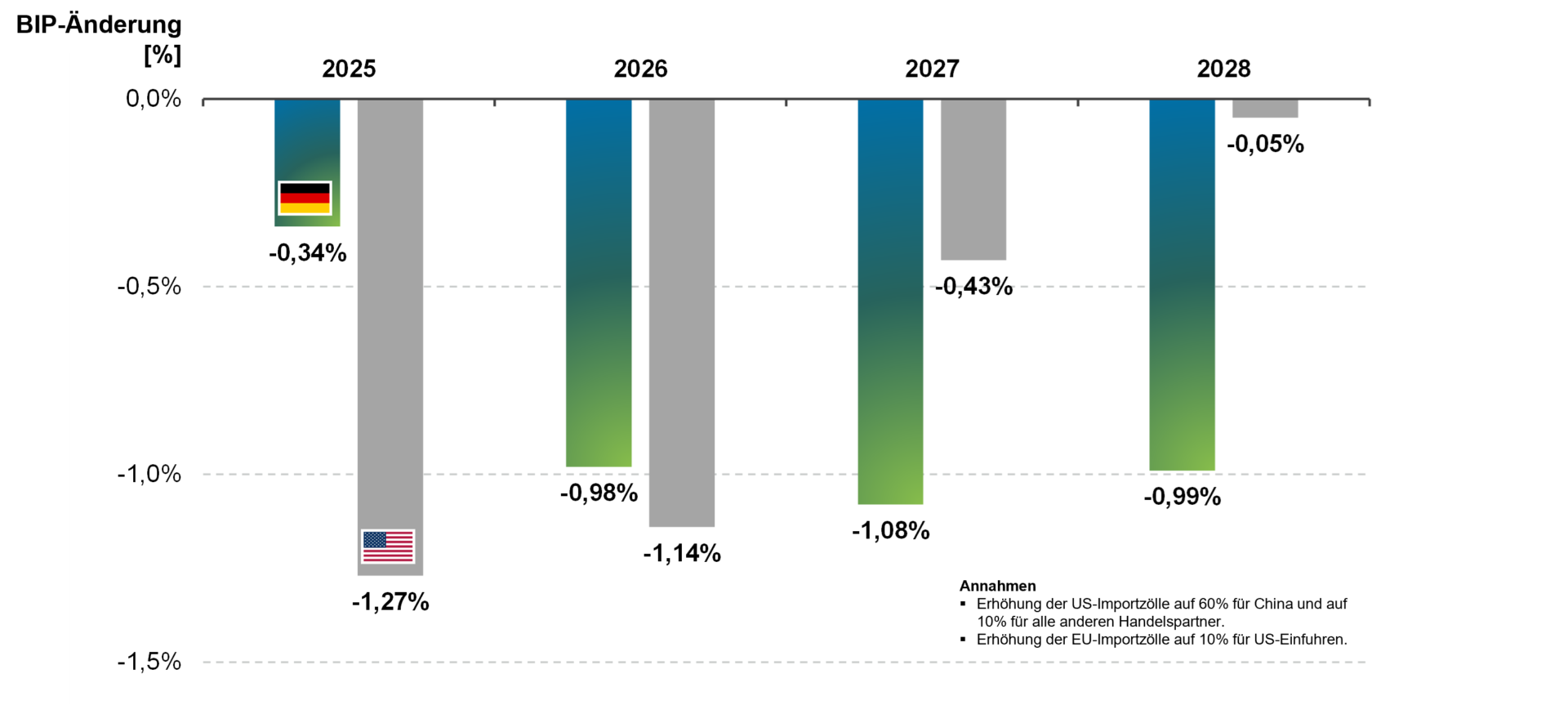

The tariff increases threatened by Trump could have a significant negative impact on Germany’s gross domestic product by 2028. Although the economic impact of such measures will be felt by all countries involved, the German economy would suffer more than the US economy in the medium term. Despite an initial decline in economic output, model calculations show that the US economy will recover almost completely by 2028, while Germany would have to accept a significant decline in gross domestic product in the long term. Over the period from 2025 to 2028, the cumulative GDP losses add up to EUR 180 billion(source).

The transactional and volatile trade policy under Trump is creating uncertainty and could delay investment decisions in Europe and Asia. Companies could become more cautious with long-term projects as they fear rapid or unfavorable changes to the framework conditions. Stricter trade measures could also unsettle investors and cause capital outflows from Europe, resulting in higher financing costs. The German mechanical engineering sector, which traditionally plays a leading global role in the development and production of capital goods and sells a large proportion of its products in Europe and Asia, would be particularly affected.

Trump’s volatile trade policy threatens investments, supply chains and prices in Europe and creates additional uncertainty for companies through tariffs, regulation and exchange rate risks.

Dr.-Ing. Oliver Lücke, Senior Advisor

The unpredictability and short-term nature of Trump’s decisions could trigger considerable uncertainty and increased volatility on the financial markets, particularly in the key EUR/USD and CNY/USD currency pairs. Unsettled markets could steer capital flows to the “safe haven” USA, which would further strengthen the dollar in addition to the protectionist measures. This could in turn lead to rising commodity prices and higher hedging costs.

If Trump increases import tariffs in the USA for certain product groups, affected foreign companies will look for new sales markets to compensate for the losses in US business. Chinese companies in particular could increasingly focus their activities on the European market. Such an oversupply could lower prices for industrial goods in Europe in individual sectors. This would severely affect German industry, which generates around 75% of its sales within the EU (including domestic sales in Germany) and is therefore particularly susceptible to an intensified price war.

As part of his “America First” strategy, Trump could further tighten the existing provisions of the “Buy America Act” and the “Inflation Reduction Act”, particularly with regard to local content requirements for government contracts, and extend them to additional classes of goods. In his first term in office, Trump also used national security as an excuse to specifically exclude individual foreign companies – such as Huawei – from the market.

President-elect Trump plans to strengthen domestic production and create new industrial jobs in the US. These plans not only present challenges, but also open up opportunities for European industry.

Trump is aware that foreign investment also plays a decisive role in strengthening US industry. The tax benefits announced are therefore generally aimed at local value creation, so that European industrial companies can also benefit from tax advantages if they relocate production to the US. In addition, government subsidy and support programs for industrial investments are likely to be further improved and made more attractive. Furthermore, simplified bureaucratic procedures and faster approval processes could provide additional incentives to invest in the US market.

The USA is already one of the industrialized countries with the lowest energy prices in the world. Trump’s deregulation of the energy sector should help to further reduce these costs or keep them at a stable low level. Energy-intensive sectors in particular, such as the chemical industry, could benefit from this development by expanding production capacities in the USA. Companies could also benefit from a more stable energy supply and a lower risk of energy policy regulations compared to Europe.

At this year’s symposium of the German Association of Materials Management, Purchasing and Logistics(BME), there was a consensus among the experts: the expected tariffs under a Trump administration are likely to significantly restrict the US business of Chinese suppliers. The resulting overcapacity in Chinese industry could lead to noticeable price reductions in purchasing in the short term. German industry in particular, which relies heavily on China as a procurement market and has well-organized purchasing teams, could use this development to achieve cost advantages and thereby strengthen its position against its competitors.

The planned expansion of US industrial production under the future Trump administration will significantly increase demand for production resources and modern infrastructure. Manufacturers of high-quality machines, innovative automation technology and sustainable technologies in particular can benefit from this. In addition, the growing demand for specialized software solutions opens up opportunities for European suppliers who provide innovative technologies to increase efficiency and digitalization.

The infrastructure programs initiated under the Biden administration are likely to be continued or even expanded under Trump. This will create additional sales opportunities for European manufacturers of construction machinery, building materials and tools, provided they have an efficient distribution network and meet the local content requirements that are sometimes demanded. At the same time, new major projects in the areas of transport infrastructure, energy supply and broadband expansion could create additional demand, from which European technology suppliers could also benefit.

Trump’s policy creates opportunities for European companies: Tax benefits, low energy prices, purchasing advantages in China, infrastructure and industrial programs offer potential for investment and growth.

Dr.-Ing. Kai Philipp Bauer, Senior Manager

The forthcoming Trump administration will pose considerable challenges for the supply chains of European industry, but will also open up a wide range of opportunities. In order to take advantage of these and counter the risks, European industrial companies must adapt their supply chains strategically and with foresight to the new framework conditions.

Establishing production capacities in the USA enables European companies to benefit from tax advantages and local subsidy programs and to avoid customs duties. Local production strengthens the competitive position and secures market access, especially with increasing local content requirements. At the same time, companies can expand their proximity to important customers and benefit from lower energy costs and political support for domestic industry. This minimizes risks due to trade barriers and creates long-term planning security in the world’s largest single market. Localization requires, among other things, BOM structures that simplify local product specifications and localized procurement.

Cooperation and joint ventures with local US companies offer a strategic opportunity to secure market access and better fulfill regulatory requirements such as local content. European companies benefit from the knowledge and networks of their partners, which makes it easier to adapt to specific market requirements. In addition, such alliances strengthen innovation as they promote access to new technologies, expertise and resources. Especially in high-growth sectors such as automation technology or sustainable technologies, such partnerships can be a decisive competitive advantage.

The targeted development of expertise in customs and transport is a decisive lever for minimizing risks from trade barriers and new regulations. Specialist knowledge of customs procedures, import and export regulations and precise logistics planning can help to avoid potential cost increases due to customs duties and delays. In addition, optimized transport logistics enable supply chains to be secured in the event of global disruptions. Investing in training, digital customs clearance and collaboration with experienced logistics partners boosts operational efficiency and gives companies a competitive edge in an increasingly complex international trade environment.

Comprehensive risk management is essential to counter uncertainties caused by protectionist trade policies and volatile markets. Companies should analyze scenarios, develop alternative procurement strategies and focus on diversifying their suppliers. In addition, early warning systems can help to identify geopolitical risks or regulatory changes in good time. The use of digital tools and real-time data makes supply chains more transparent and flexible, which significantly improves the ability to react to unexpected disruptions.

In order to counter the increasing price pressure in Europe, targeted cost-cutting programs can increase competitiveness. Optimizations along the entire value chain, for example through automation or lean management approaches, offer potential savings.

Due to sustained growth, companies have also built up structural costs, which is why a particular focus should be placed on the indirect area. Strategic purchasing advantages due to overcapacity in markets such as China can also be used to source raw materials and preliminary products more cheaply. A clear focus on efficient processes and innovative products strengthens the market position despite tougher competition.

Natural hedging reduces exchange rate risks by planning income and expenditure in the same currency. The expansion of production capacities or supplier networks in the USA and Asia can help to minimize currency risks and stabilize costs. This strategy not only increases financial planning security, but also strengthens local presence and market ties. Especially in volatile currency environments, natural hedging is an effective means of cushioning economic fluctuations.

A resilient supply chain is characterized by flexibility, diversification and robust risk management. Companies should develop alternative procurement and sales markets, build up redundant capacities and digitalize processes. A proactive approach to supply chain planning and optimization increases resilience. By investing in transparent data flows and agile structures, disruptions can be minimized and response times shortened, creating competitive advantages in the long term.

Take advantage of the opportunities and meet the challenges of the new trading conditions with an optimized supply chain. We will be happy to help you develop solutions together that will make your company future-proof.

Dr.-Ing. Kai Philipp Bauer, Senior Manager

Senior Manager

Would you like support in future-proofing your company? With our expertise, we are happy to help you develop innovative solutions and optimally align your supply chain to new trading conditions. We are also at your side as a competent partner during implementation.

Senior Manager, Hamburg

Kai Philipp Bauer studied mechanical engineering with a focus on production technology and has been working in consulting for over 15 years. He advises his clients in particular on issues relating to strategy development, operations management and digital transformation.

Senior Advisor, Hamburg

Oliver Lücke studied mechanical engineering with a focus on production technology. After 25 years of operational supply chain responsibility as a senior executive, he now works as a lecturer and consultant for SCM. He supports companies and managers in taking their supply chain management to the next level, both technically and economically.

We show you the best US production locations for mechanical engineering, chemicals, automotive & high-tech.…

Sustainability in operations not only offers the opportunity to make a positive contribution to society…

Have you ever heard of Kanban? Sure! Have you already established the method for C-parts…

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Turnstile. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Facebook. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from Instagram. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More Information